Letter to Investors Q1

The start of our first quarter has been exceptionally eventful, both for our firm and the world at large. Uncertainty is once again upending the markets. While history does not typically repeat itself—as Howard Marks often notes by quoting Mark Twain—it certainly does rhyme.

Key Events This Quarter

1. The AI Security Disruption - 20 Feb 2026

Anthropic released Claude Code, sending shockwaves through the cybersecurity world. Beyond demonstrating superb coding abilities, the model autonomously discovered several security vulnerabilities. In an immediate overreaction, investors essentially declared most SaaS models obsolete. The market assumption was that non-tech companies would now risk having their limited IT teams "vibe code" enterprise-grade cybersecurity defenses or complex workflow software.

While anything is possible, I do not believe a company like McDonald's will establish an internal IT team to develop proprietary defenses against advanced cyber threats, investing capital in non-core capabilities. They are far more likely to hire CrowdStrike or others. However, non-mission-critical, everyday office productivity software could indeed be easily replaced.

2. Geopolitical Escalation and Supply Chain Shocks - 28 Feb 2026

The outbreak of conflict involving the US, Israel, and Iran led to the closure of the Strait of Hormuz. This effectively halted ~20% of the world's crude and LNG exports, alongside ~33% of global fertilizers and sulfur exports, and ~10% of refined aluminum and petrochemicals exports. The conflict caused significant damage to Qatar's natural gas and critical infrastructure, guaranteeing a lasting impact on global supply.

Asia and the EU are bearing the brunt of this disruption. The US, as the world's largest fossil fuel producer, is likely to experience only temporary price hikes. More importantly, Qatar holds roughly 33% of the world's helium — a byproduct of LNG and a critical component in semiconductor manufacturing — while the US produces another ~50%.

This dynamic creates two critical outcomes that disproportionately benefit the US:

US Manufacturing Ambition: Increased input costs outside the US will serve as a tailwind for America's renewed ambition to rebuild its domestic manufacturing hub.

Strategic Resource Control: With the loss of Middle Eastern helium supply, China and other Asian nations will be forced to rely heavily on the US, severely tilting the balance of power in critical resource negotiations.

3. The Advent of Agentic Warfare - 7 Apr 2026

The release of Mythos Preview sent a secondary shockwave through the tech industry. By demonstrating the ability to autonomously generate cybersecurity attacks, it validated the arrival of comprehensive agentic capabilities. This development holds profound implications for the future of warfare and national security, evoking memories of the 2010 Stuxnet attack on Iran. Given its immense significance, navigating this shift will be the primary focus of our future investment strategy.

Assessing Claude Mythos Preview’s cybersecurity capabilities

AI Just hacked one of the world’s most secure operating systems

Stuxnet, a 2007-2010 event provides some prelude

https://www.theguardian.com/technology/2010/sep/30/stuxnet-worm-new-era-global-cyberwar

2026 Market Outlook

1.0 AI Development

The creation of autonomous agents is a natural progression in AI development. The intent has been on display for a decade, most notably as engineers and scientists pushed to develop self-driving vehicles.

Like all tools, AI is immensely useful when governed appropriately, yet potentially devastating when deployed with ill intent. Consider the invention of the cooking knife or the harnessing of fire: with proper governance and sensible enforcement, humanity enjoys culinary masterpieces despite the occasional, severe consequences of misuse. The convergence we are seeing today is entirely in line with expectations, driven by surging computing power and algorithmic breakthroughs. Naturally, if an agent is instructed by a bad actor, chaos should be expected. While these agents can construct and successfully execute credible plans, the underlying intent still requires a human trigger.

While frontier models are significantly more capable and genuinely astonishing, they remain the result of probabilistic engines. They are trained on trillions of parameters derived from human publications, augmented by the exponential growth of simulated, reinforcement-learning data points. Humans remain the constant link.

Consider this: Salted caramel chocolate wasn't a mainstream flavor before 2008. In fact, salted caramel itself was not "invented" until 1977 by chocolatier Henri Le Roux, despite salt, sugar, butter, and chocolate existing side-by-side for thousands of years. It took another three decades for it to become a global phenomenon.

The genesis of flavors like salted caramel and chocolate, emerging from serendipity, collaboration, and intuition, is still beyond current probabilistic AI models. Any such non-conforming notion would be considered a hallucination. Human feedback and refinement of AI output will continue to shape these models to produce results that are generally accepted, rather than another favorite like salted caramel chocolate.

We are also not surprised by Anthropic's ability to discover 27-year-old software vulnerabilities that remain unpatched. This is not a grand "aha" moment. Uncovering flaws left behind by five decades of sloppy programming across billions of lines of code shouldn't surprise even a novice programmer. It does, however, represent a massive opportunity for existing cybersecurity experts, refuting the naive assumption that merely "vibe coding" can produce enterprise-grade security solutions.

To put things in perspective, CrowdStrike's ability to detect and defend stems from its superlative pattern-recognition capabilities built from the start. CrowdStrike's Falcon platform processes over 100 billion security events per day as of mid-2024, making over 2.3 million decisions every second - around 200 billion decisions a day autonomously, a type of AI. It is not the famous LLM that consumers are familiar with, but a specialised cybersecurity model that can act autonomously and is trusted by many enterprise users.

This is still not AGI. It is reproducing and synthesizing what it has learned.

It is certainly more powerful than anything we have seen, possessing an incredible ability to recall and organize information at breakneck speed. It works tirelessly without complaints, holidays, or a need for work-life balance. However, it still lacks true contextual understanding, humanity, empathy, ethical intuition, and the genuine spontaneity of the human mind.

Adoption, nevertheless, is an absolute necessity.

Human Development

Human development is a must.

That said, relying entirely on AI for critical thinking from a young age may impede cognitive connectivity and hinder brain development. Overreliance could dull the experiential learning necessary to cultivate instinct. Generations who navigated the world using physical maps and landmarks developed a far superior internal compass compared to those glued to GPS, who often panic the moment they lose a signal. Until true AGI arrives, human knowledge and experience remain invaluable. An experienced architect wielding AI will design a vastly superior home than a layperson using the exact same AI model. With a sufficiently trained mind and deep experience, AI becomes a superb tool, enabling individuals to achieve remarkable things in this new era.

While we strongly believe hardware supply continues to lag substantially behind actual market needs, the expectation that software companies will be entirely eradicated is far too simplistic. A substantial number of software companies perform highly specific functions that non-technology companies simply do not have the bandwidth, expertise, or shareholder mandate to internalize. Infrastructure software and cybersecurity are prime examples of sectors unlikely to be disrupted—unless they fail to anticipate the escalating challenge of malicious AI threats. Consequently, we have distinctly bucketed companies into "enablers" and "disrupted" within our investment framework.

We remain steadfast in our belief in technology investing. But new governance is urgently needed, and it remains glaringly absent.

(As a side note: China has been noticeably quiet. There are countless Chinese AI scientists working in Silicon Valley. Is China lagging significantly behind in this specific race, or are they simply observing the ingenuity of US development in awe?)

1.1 AI Governance

Anthropic's red team is confident that the defenders—the "good guys"—will ultimately come out on top. We share that belief.

In recent months, the market seems to have entirely discounted years of foundational work by cybersecurity companies, acting as if the industry was caught completely unaware by the risks posed by AI agents. What some investors fail to realize is that AI governance and defensive AI capabilities have been central topics at cybersecurity conferences and on CEO agendas since as early as 2019. While these frontier models were achieving incredible milestones at lightning speed, cybersecurity firms were quietly working alongside their largest enterprise clients to develop governance rules and defensive perimeters.

On April 6, 2026, CrowdStrike outlined its collaboration with Anthropic, detailing a clear division of labor to provide clients with optimal security solutions. Governments and enterprises require robust, continuously evolving capabilities to defend against bad actors wielding AI, just as they do against traditional cyber threats.

I have no doubt that elite cybersecurity firms will increasingly focus their defensive perimeters at the OS kernel level, rather than merely monitoring the web-connected ports of endpoints and servers. We should also expect a significant strengthening of authentication protocols and the delegation of authority from endpoint instrument providers.

Simultaneously, governments must establish coherent policies, guardrails, and stringent enforcement mechanisms. Without sensible rules of the road, the proliferation of the AI of Things (AIoT)—including consumer robots, autonomous vehicles, and industrial applications—will be severely bottlenecked.

1.2 AI and the Future of Living

The "Future of Living" will be dominated by AI applications across all facets of life and work. How exactly will this transformative technology alter our daily reality?

Why is this time different?

Over the last century, governments and the defense industry possessed the exclusive resources and capabilities to innovate. Typically, they kept these advancements to themselves for decades. GPS, for instance, was invented by the US Department of Defense in 1973 but didn't reach mainstream consumers until the early 2000s. The Internet followed a similar trajectory.

The traditional progression was predictable: government adoption, followed by massive commercial defense contractors, eventually trickling down to the consumer market years later. Because these technologies were initially exorbitant, companies enjoyed a long runway to generate profits and recoup R&D investments before lower-cost iterations reached the public.

AI proliferation, however, flipped this script entirely. It started directly with consumers—often via freemium or low-cost models—leaving analysts puzzled over how the trillions of dollars currently being invested will ever be recovered. ChatGPT reached 1 million users in five days. While it was fraught with hallucinations in 2023—justifying the skepticism of traditionalists—the exponential improvement over a short three-year span has been staggering. The pendulum has swung so violently that humanity now genuinely fears the capabilities of models like Mythos Preview. Nothing of this nature has happened before.

Today, no software engineer works without an AI assistant, and no Nvidia engineer designs hardware without one. The newest Anthropic models are refined using AI assistants themselves.

Meanwhile, younger generations entering the workforce are adopting these tools frantically, while a significant cohort of mid-to-late-career white-collar workers watches with a mix of suspicion and disconnect. Many corporations are attempting to bridge this gap by sending employees to "AI night schools." Yet, despite these efforts, an MIT report suggests that 95% of non-tech companies attempting to integrate AI use cases fail to generate positive financial returns. This is likely because their legacy IT teams lack the specific vocational skills required to successfully architect AI into existing business workflows.

As high-tech giants like Microsoft and Meta continue to optimize and trim their workforces, displaced technologists will inevitably find their way into traditional Fortune 500 companies desperate to implement AI. This transition will absorb tech-sector unemployment but will likely freeze non-tech hiring, resulting in a bleak job market for fresh graduates from non-technical disciplines.

Furthermore, the "experienced hands" within these traditional companies will be retained. Their deep, undocumented understanding of business processes is required to help new technologists build bespoke AI systems (their own "Jarvis"). More importantly, human experience acts as the ultimate, instinctive guardrail against algorithmic mishaps.

Ultimately, we foresee three macroeconomic outcomes:

Secular Decline in White-Collar Employment

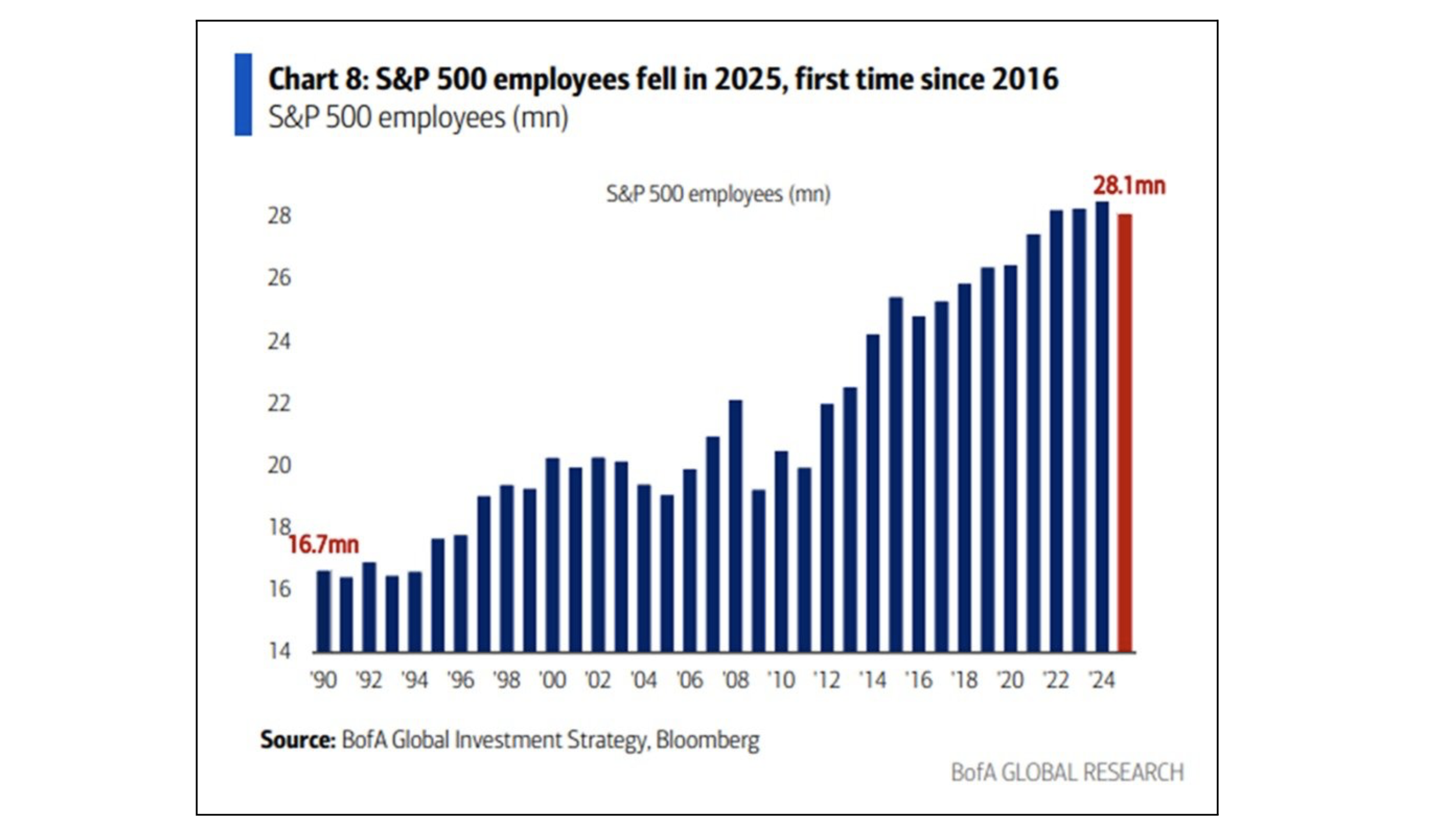

White-collar employment will shrink. This will not be a sudden cliff-edge event, but a slow, secular decline. New hires will be sparse. As Federal Reserve Governor Christopher Waller noted recently, the US economy has performed well but is generating little to no increase in actual employment. Corporate cost structures will fundamentally and permanently shrink. BofA Global Research's chart clearly demonstrates the start of the secular decline.

Wage Deflation and Lower Consumption

Rising unemployment and stagnant hiring will logically lead to lower aggregate consumption power at today’s price levels. Deflation in wages and consumer prices will likely emerge as the new secular trend. Consider the modern entertainment experience: today, one can watch a full-length feature film at home in high definition on a near-free streaming subscription, accompanied by a premium $5 craft beer. Decades ago, this same experience cost $50 at a theater. High-quality products and services are already fundamentally cheaper to produce and distribute.

Innovation and productivity lead to better products at lower costs

Only firms with genuinely innovative products and a relentless focus on cost management will survive a macro environment where consumer income is pressured. If given the choice, consumers will maintain their volume of consumption, but only at lower prices.

As businesses fight to survive, they will find themselves stripped of pricing power. Large enterprises and those armed with disruptive technologies possess the efficiency required to lower prices and maintain volume. Margins will inevitably suffer, leading to widespread closures. Consequently, the "winner-takes-most" phenomenon will become increasingly pronounced and concentrated—crucially, without driving new human employment in the process.

Any government intervention designed to shield national champions from foreign competition is ultimately an exercise in futility. As Michael Porter would likely attest, protectionism merely disadvantages a nation's citizens whilst blunting its own competitive edge.

Tesla and BYD have effectively put this theory into practice. They have engaged in a relentless battle for market share by continuously driving down prices since 2023. Tesla managed to challenge the highly efficient BYD only by leveraging its own full-stack manufacturing capabilities in Shanghai.

Elon Musk proved that such hyper-efficiency is attainable, and his experiences have likely instilled in political leaders like Donald Trump the confidence that reshoring is both necessary and viable. However, investors must look past the political rhetoric. This shift toward reshoring is not a social programme designed to generate millions of high-paying union jobs, as President Biden often suggests. Rather, the objective is to build highly automated facilities that will employ a fraction of the workforce seen in traditional GM or Ford plants, producing desirable goods at a significantly lower cost than the US can manage today.

Unable to compete on these new terms, legacy Western automakers have grown understandably anxious. Lobbying governments to ban Chinese EVs under the pretext of "overcapacity"—even whilst domestic Chinese consumers wait months to take delivery of their vehicles—is akin to an ostrich burying its head in the sand. Many of China's most popular models have not yet even reached the international market. Furthermore, those that are exported are often sold at higher gross margins than they command domestically. It is little wonder, then, that figures like Janet Yellen prefer the diplomatic term "overcapacity" rather than accusing them of "dumping."

Conversely, Tesla's blended global cost structure has made its vehicles affordable enough to sustain profitability amidst these price wars. Imagine, for a moment, if Tesla were solely manufacturing within the US; its fate would likely mirror that of Ford, General Motors, and Stellantis, who are currently scaling back their EV ambitions.

Apple provides the ultimate blueprint for this era. They pour billions into R&D. The iPhone 17 is undeniably vastly superior to the iPhone 15, yet the launch price remained identical. Apple has masterfully kept its Cost of Goods Sold (COGS) growth lower than its revenue growth for over a decade. While Global GDP grew 49% (from $77T to $115T) over the last ten years, Apple’s revenue grew 86% (from $230 billion to $435 billion), and its EPS exploded by 223% (from $2.31 to $7.46). Investors rewarded this operational genius with an 821% stock appreciation.

People buy products that are exceptional and affordable. Moving forward, the nation and the region that can engineer the most efficient, AI-integrated supply chain will unequivocally win the race.

1.3 AI Landscape and Road Map

Foundation Model Builders

Foundation Models: The class is very crowded with top students with big pockets or big scholarships. Google’s Gemini, DeepSeek, OpenAI, Anthropic, Qwen by Alibaba, Mimo by Xiaomi, Zhipu AI, Grok by xAI, Llama by Meta…. And more.

The current leader in the AI foundation model race is Anthropic, with a 1-trillion-parameter model, Mythos, that can autonomously generate code to complete tasks humans instruct it to. OpenAI and Google are not far behind. Leadership will change, I am sure of it, like all marathon races.

To win, more capital expenditure would be needed. Companies with the right talent, strong free cash flow generation, or cult-like wealthy investors following can stand a chance to lead the race. The capex this year would be north of $600 bilion. More next year.

Why does this make sense? The combined revenue expectations for OpenAI and Anthropic are possibly only $50 billion in 2026!

Because technology diffusion did not start at the government and enterprise levels but at the low-fee-paying consumer market, analysts are having a tough time estimating how much enterprises would pay for such technological marvels.

We are now witnessing a move up the food chain as more enlightened enterprises find ways to adopt it. Many would end up paying top dollars for the services as they recognise the need to compete. Anthropic's focus on enterprises and premium AI builders is well-placed to take more enterprise market share.

Commercialisation

Enterprise adoption remains in its infancy. Last year, an MIT study revealed that 95% of surveyed companies had failed to define proper use cases or derive tangible financial benefits from their AI initiatives. We believe this dynamic is shifting dramatically as displaced technologists migrate to traditional enterprises to spearhead AI deployment. Consequently, we anticipate three primary developments:

A Surge in Adoption and a Deficit in Compute: AI adoption will accelerate substantially throughout 2026 and 2027. We project a severe shortfall in computing power, memory, and storage required to meet surging enterprise demands for model training, refinement, and inference. As newer models engage in more complex "thinking" and planning, their compute requirements will increase exponentially. This explosive demand for token generation will create immense economic value amidst constrained supply, granting leading AI firms significant pricing power.

Value-Based Pricing Models: AI providers will likely adopt a bifurcated pricing strategy. They will charge enterprises an affordable rate for "input tokens" (the prompts), whilst charging a substantial premium for "output tokens" (the generated solutions), correctly identifying that the output is where the true economic value is crystallised.

Expanding Threat Surfaces and the Cybersecurity Boom: As commercialisation flourishes, the digital threat surface will inevitably expand. Enterprise networks will require advanced "security guards" armed with the latest defensive AI capabilities. Heightened risk awareness will drive substantial revenue from corporate clients, funding cybersecurity firms to develop ever more sophisticated defensive perimeters.

Application layer

The development of application libraries tailored for industrial use is of paramount importance. Nvidia, Google, and other major AI companies have created application libraries with industrial foundation knowledge that will allow non-tech enterprises to adopt quickly. By combining them with their own enterprise data, an enterprise can turn these industrial foundation models into subject-matter experts. For example, banks with a wealth of credit and operating account data can train an AI with this data, and subsequently assess any new credit applicant's creditworthiness. With the help of newly hired mega-cap tech veterans, they led their firm to adopt AI with a foundation model that would provide traditional enterprises a crucial head start. Successful enterprise adoption will drive productivity by optimising workflows, eliminating human bottlenecks at key decision nodes, and hyper-personalising products and services for individual consumers. Ultimately, it is a mechanism for structurally reducing cost and waste.

It is not difficult to envision a near future in which every enterprise becomes a massive consumer of token generation - both for inference and for continuous feedback via reinforcement learning - simply to maintain a competitive edge and sustain client engagement. This paradigm shift will require substantial inference infrastructure and dedicated "AI factories" aimed at continuous model improvement, operated either in-house or outsourced to hyperscalers.

This virtuous cycle of investment and deployment will likely run for several years before reaching equilibrium. Consequently, the insatiable demand for these AI factories will fuel the exponential growth in hardware requirements.

Hardware Infrastructure

Hardware battleground

US firms undoubtedly lead in chip and server design, producing significantly more tokens per kilowatt. However, the capital expenditure required to build an AI factory or a neo-cloud data centre in the West is 50% to 100% higher, takes considerably longer to complete, and incurs vastly higher ongoing electricity costs compared to their Chinese counterparts.

While China may currently rely on more power-hungry servers and chips that run at slower speeds than those available in the US, this disadvantage is offset by three structural realities:

Execution and Supply Chain: Unparalleled construction capabilities and a deeply integrated domestic supply chain.

Energy Abundance: Over twice the power generation capacity of the US. A substantial and growing proportion of this is derived from green energy (China produces more renewable electricity than the next two nations combined), underpinning a robust self-sufficiency strategy.

Engineering Resilience: Chinese technologists thrive in a cutthroat, highly competitive environment, possessing superb application engineering abilities honed through rigorous education and relentless practical experience.

Consider Huawei’s CloudMatrix 384, completed in April 2025. This was the first large-scale silicon photonic network designed to bridge the compute shortfall with exceptionally high network speeds. Running on the QingTian architecture, it features zero-loss, low-latency scheduling and highly optimised Compute Architecture for Neural Networks (CANN) software to maximise AI performance. China’s resilience consistently demonstrates a core truth of technological development: there is always another way. Technological chokeholds and sanctions are, historically speaking, only ever temporary.

Ultimately, regardless of national borders, the economic output of these AI factories is universally required. Sovereign states and their enterprises will make their own choices, building or renting this infrastructure simply to maintain a competitive advantage and avoid obsolescence. Both China and the US are clearly well-positioned to serve as the world's primary AI token exporters. No other nations possess the unique "technological genetics" and scale required to compete at this level. The countries endowed with these structural advantages will capture the lion's share of next-generation economic growth, much as crude oil enriched Saudi Arabia and the Middle East a century ago.

Hardware longevity

Not every enterprise can afford the staggering capital outlay required to build its own neo-cloud data centre. The vast majority will ultimately rent compute. Naturally, most will desire access to Nvidia's upcoming Vera Rubin architecture via their chosen hyperscalers. However, due to constrained supply, only top-tier clients will likely secure meaningful allocations.

As Jensen Huang famously remarked, "The more you buy, the more you save." The reality of this market dictates that unless an enterprise is already a top-paying customer for the hyperscalers, they will find themselves at the back of the queue. Few possess such deep pockets.

Counterintuitively, this dynamic guarantees the longevity and rentability of older-generation chips. As the commercial adoption of AI accelerates, the sheer demand for compute will precipitate an acute shortage. We expect this to act as a floor for the rental prices of legacy chips, potentially even driving yields higher—a phenomenon we previously observed during the 2018–2020 cryptocurrency boom.

Second-Order Risks in Private Credit

Does this sustained demand provide a margin of safety for private credit investors heavily exposed to the neo-cloud sector? What about the opaque, off-balance-sheet structures that hyperscalers and mega-cap tech firms increasingly employ to fund their data centres and power generation facilities in partnership with private credit firms?

Furthermore, if legacy software firms face severe disruption from agentic AI, how will this impact their ability to service their own debt burdens? Would that affect the older data centers?

These are the second-order risks we are monitoring closely. Just as we scrutinised commercial real estate (CRE) risks in 2022, we must look beyond the immediate thematic beneficiaries. However, unlike the isolated nature of certain CRE distress, the financial linkages in the AI infrastructure build-out are far more systemic.

Energy and the Middle East

Energy feedstock for power generation is critically important. JPM’s Michael Cemblast, in his Mar 2026 “Eye on the Market”, had an in-depth look at the world’s energy reliance on the Straits of Hormuz. He concluded that the US and China are both more than 70% insulation of the Middle East. Crucially, China's historical dependence on imported fossil fuels has steadily declined over time, driven by the aggressive, widespread deployment of electric vehicles and renewable energy infrastructure.

2.0 Economic Outlook

The war on Iran will have a significantly greater impact on Asia and put the US in an advantageous position.

Reshaping Global Manufacturing: The conflict's impact on Asian energy supplies and pricing will inevitably export inflation into manufactured goods. A prolonged closure of the Strait of Hormuz fundamentally impairs the price competitiveness of Asian exports. In severe scenarios, production may halt entirely as vital inputs - such as petrochemicals - become prohibitively expensive or wholly unavailable. This “well-planned second-order” dynamic serves as a powerful catalyst accelerating the US ambition to reshore manufacturing.

Rare Earth vs Inert Gas: The Hormuz closure chokes off the supply of helium, aluminum, and petrochemicals, all of which are the lifeblood of the Asian semiconductor manufacturing industry. Because the US is the world's largest producer of helium and petrochemical feedstocks, this supply shock effectively tilts the balance of power, giving the US unprecedented leverage at the negotiating table to counter China's dominance in the rare-earth trade.

Energy Self-Sufficiency and Regional Divergence: Both the US and China are far less dependent on the Strait of Hormuz for their energy needs than the EU, Japan, South Korea, Taiwan, and the broader Southeast Asian (SEA) region.

The Impending Asian Economic Slowdown: The final vessels to leave the Middle East in late February are only now arriving at Asian ports. When no further shipments follow, the true severity of the supply shortfall will surface. Thus far, Asian markets have remained notably sanguine. This complacency is somewhat understandable - this is not a COVID-era supply shock, and markets have largely digested Trump’s reaction function to the voters of the stock market. However, restoring production to pre-war levels will take way longer than six months once the straits reopen.

Elevated costs for energy, petrochemical feedstocks, fertilisers, helium, aluminum, and other industrial inputs will act as a heavy tax on Asian economies, likely resulting in a 0.5% to 0.8% slowdown. Supply chain preparedness will be severely tested in May. Meanwhile, the US, as the world's preeminent fossil fuel producer, is perfectly positioned to step in as an alternative supplier to Asia - at a premium price, naturally.Tailwinds for US Equities: Historically, strong exports from Korea and Taiwan have been leading indicators for S&P 500 EPS growth. This dynamic supports our view that continued capital expenditure and reshoring efforts will generate inflationary pressures that paradoxically support margin expansion for US enterprises in the industrial and technology sectors. Furthermore, US integrated oil companies should perform exceptionally well, benefiting from prolonged, elevated refinery margins, sustained prices at the pump, and the favourable spread between domestic light sweet crude and Canadian heavy crude.

US inflation remains a concern: High gasoline prices place a direct strain on the Consumer Price Index (CPI) and erode consumers' disposable income. While retail sales (excluding energy) remained robust in March, the April data will provide a clearer picture of consumer health. Consequently, we expect the Federal Reserve to hold rates steady for the vast majority of 2026.

China’s Deflationary Consumer: While China's CPI is edging upwards, consumer confidence remains deeply depressed, and wage growth is subdued. Chinese corporations are cautious about the broader economic outlook, choosing to remain exceedingly frugal regarding wage increases and capital expenditures.

Monetary Policy Divergence and Policy Error Risks: The US may find it easier to manage energy-driven inflation, as the largest fossil fuel producer, targeted fiscal adjustments could mitigate the impact on end-consumer prices, granting the Fed the flexibility to hold rates steady or even cut if conditions ease.

Conversely, Asian central banks face a classic stagflation trap. They will likely feel compelled to tighten monetary policy in a weakening economic environment, fighting cost-push inflation driven by supply shocks rather than demand. This policy error will likely leave the broader Asian economy in a highly vulnerable position.

China is likely to fare better due to adequate advance planning regarding resource reserves. Throttling down export volumes at this juncture makes strategic sense to prevent the exhaustion of national resources. While the People's Bank of China (PBOC) has room to adjust monetary policy, it will likely favour targeted interventions over broad-based interest rate cuts. Chinese household savings reached a staggering ¥167 trillion (US$23.96 trillion) in December 2025. Even a marginal shift in household behaviour—whether towards consumption or investment—would trigger a massive economic response. Therefore, we remain optimistic that China can comfortably achieve its 4.5% to 4.8% economic growth target.Capital and liquidity conditions

We are monitoring several tightening conditions in the capital markets:The colossal build-out of data centres and power generation facilities requires an extraordinary quantum of capital. As these entities tap the debt markets at more attractive credit spreads, we expect credit spreads to widen.

Upcoming mega-IPOs will drain substantial liquidity from the equity markets. This draws parallels to 2022, when a glut of SPAC issuance, coupled with rate hikes and the Fed's balance sheet run-off, precipitated a substantial market correction. This draining of liquidity could also trigger systemic plumbing issues, particularly in Treasury futures arbitrage, which relies on abundant funding liquidity.

Incoming Chairman Walsh is not a proponent of aggressive balance sheet expansion. In the event of a market disruption, investors should not expect the Fed to ride to the rescue.

The economic conditions are also challenging. The central bank will be forced to walk a tightrope on Fed Funds rate decisions, balancing the risk of weakening employment and high energy inflation.

As the demand for goods and services rises against a backdrop of supply shortfalls, inflation expectations will firm, keeping interest rates elevated. Earnings will only improve for those companies possessing genuine pricing power. The capital markets should remain vibrant, with strong earnings in the technology and industrial sectors providing a catalyst for buoyant equity performance.

10. Economic Projection: Past data points serve no purpose, as the US-Israel Iran war has muddied the water.

For now, it is hard to see past the muddy water for a clearer macroeconomic or geopolitical outlook. We will remain nimble in our investment process.

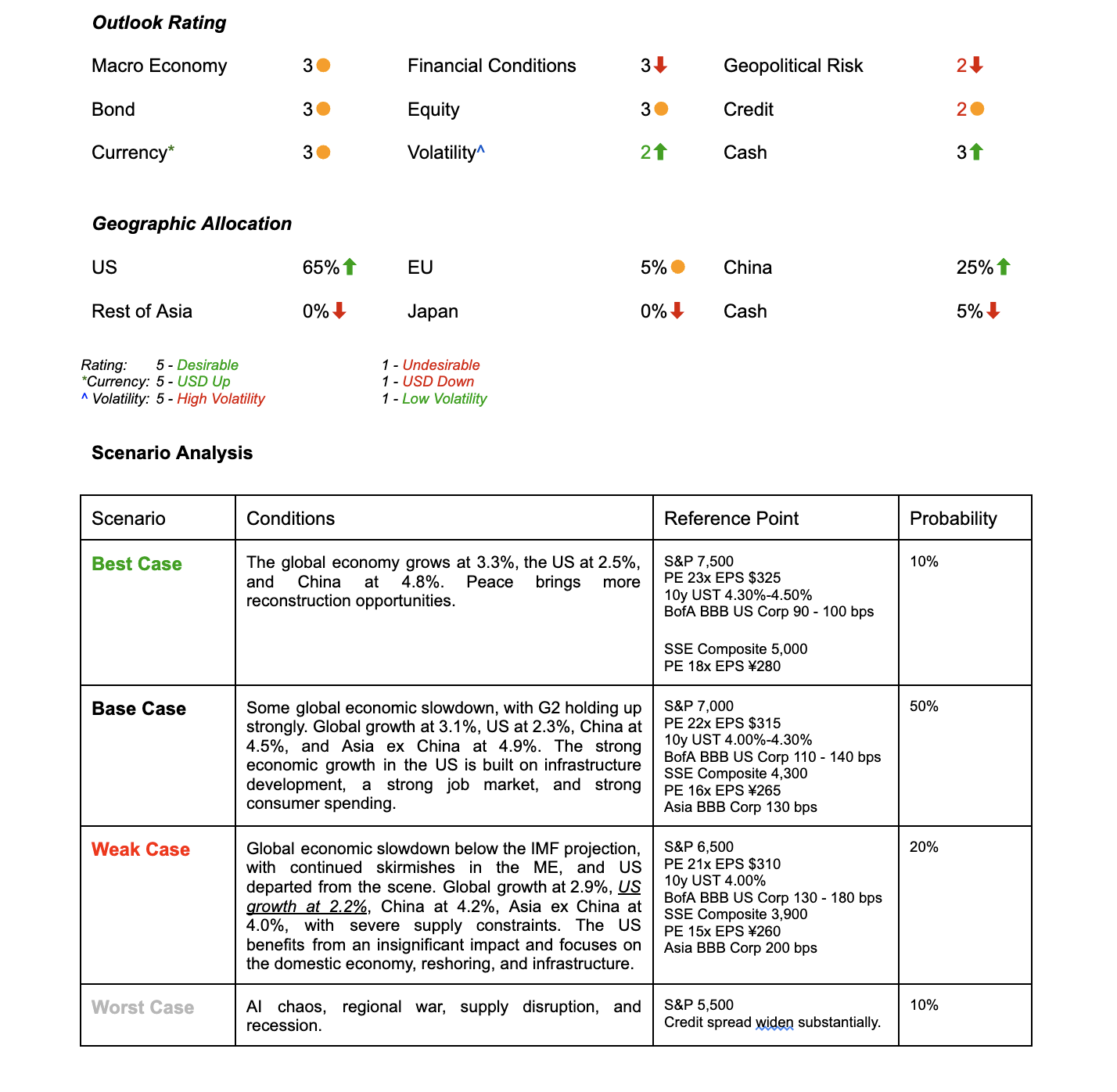

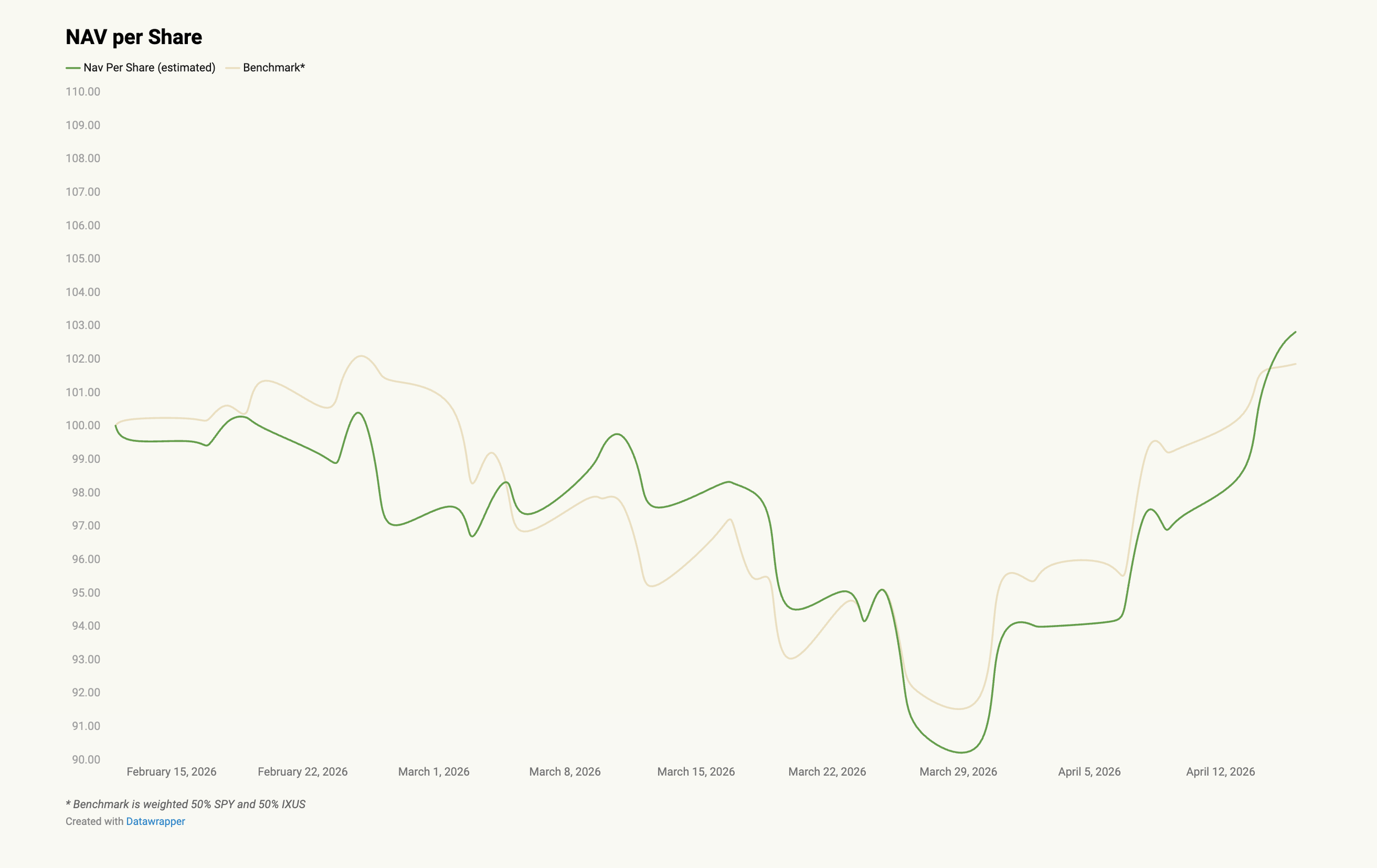

3.0 Fund Performance

Appendix: The mystery in token unit, token usage & token cost

Here, our young padawan, Joshua Dass, demystifies the concept of token economy.

The Hidden Issue: A Token Is Not a Standard Unit

Every LLM API bills in tokens - but a token is not a fixed unit of work. Each model uses its own tokeniser: an algorithm that slices text into numeric chunks before the model processes it. Because vendors control their own tokenisers, the same sentence can produce 2 - 3x more tokens on one model than another. The headline price per million tokens is therefore only half the equation - tokeniser efficiency is the invisible half, entirely within the vendor's control and largely invisible to the buyer.

Crucially, this is not fraud. The analogy is two home removal companies quoting a price per box: the cheaper rate results in a larger bill if the boxes are smaller. The burden falls on the buyer to measure the boxes - and most enterprise buyers have not done so.

How Large Is the Distortion?

The gap between list price and effective cost compounds across three dimensions.

Language: Chinese models (Qwen, DeepSeek) have larger multilingual vocabularies (~150–250k vs. ~100k for GPT-4o), so the same Chinese-language prompt consumes fewer tokens and costs less - further underscoring their apparent cost advantage over Western models.

Workload type: TensorZero ran identical inputs through each provider's token-counting API and found that cost rankings flip entirely depending on what you're sending. Claude Opus comes in at 5.3× the effective cost of GPT on certain workloads despite only a 2× list price gap, while Gemini - cheapest on plain text - becomes 46% pricier on others.

Hidden compute: Some providers bill for internal reasoning or chain-of-thought tokens the user never sees. The customer pays for compute they cannot observe or verify.

Bottom line: Published $/M token comparisons are not apples-to-apples. The only valid comparison is to run your actual prompts through each model and measure real token consumption on your specific workload.

An example: What OpenRouter Usage Data Does — and Does Not — Tell Us

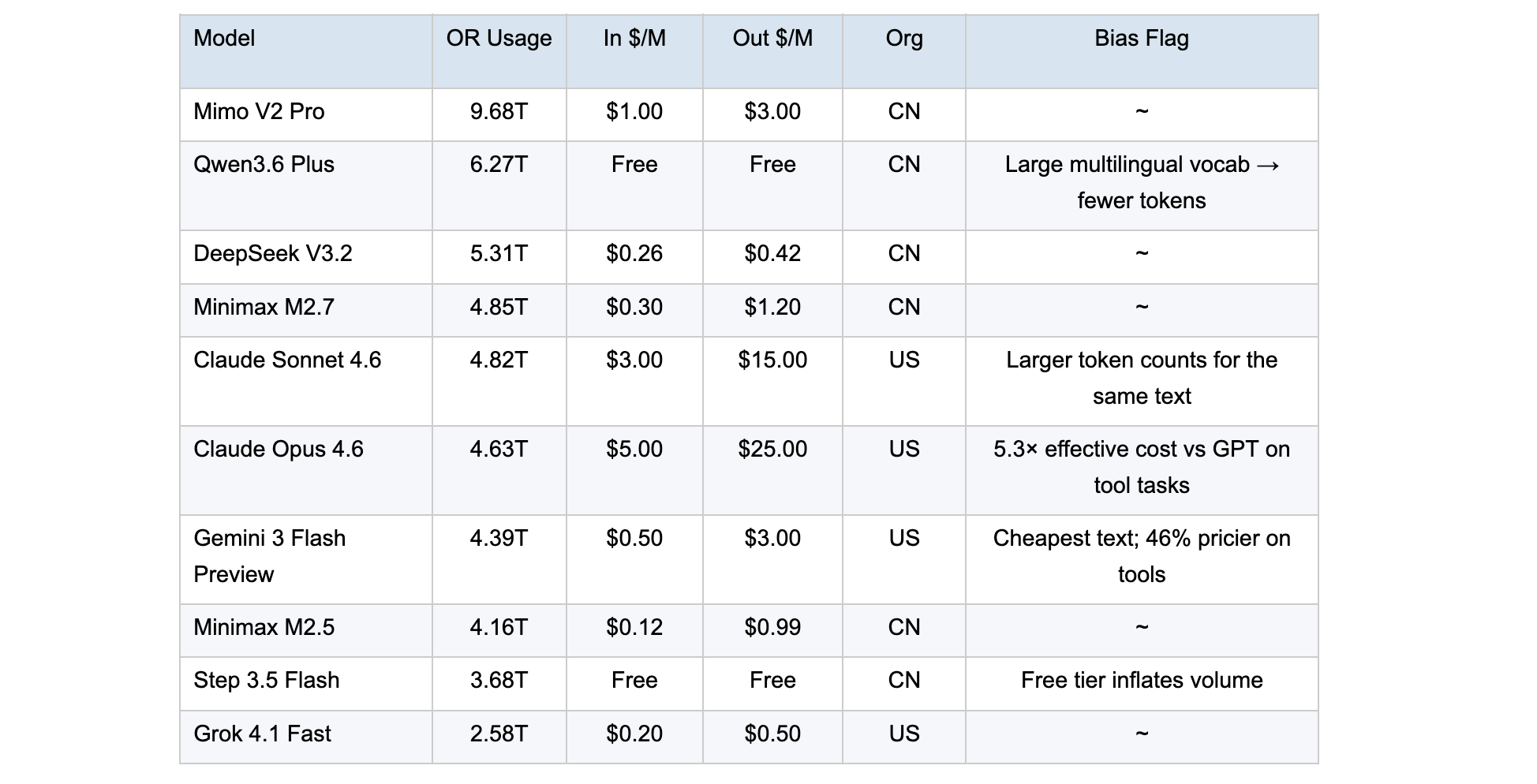

OpenRouter is a third-party API aggregation layer that routes developer traffic to multiple model providers under a single endpoint. It is popular among developers who want to switch between models without rewriting API calls, test models side-by-side, or optimise costs programmatically. The table below, citing OpenRouter data as of April 2026, purports to rank models by global token usage:

This data is subject to at least four material biases:

Sample selection: OpenRouter captures only traffic deliberately routed through its layer - primarily cost-conscious, multi-model developers. Anthropic, OpenAI, and Google each serve massive volumes of direct API and consumer traffic that are entirely invisible here. Claude Sonnet 4.6, showing 4.82T tokens on OpenRouter, likely represents a small fraction of Anthropic's total API volume.

Free model distortion: Qwen3.6 Plus and Step 3.5 Flash are listed at $0/$0. Free models attract bulk experimental and throwaway workloads that would never be run at paid rates, making their token volumes structurally incomparable to paid tiers.

Token non-comparability: Even setting aside all the above, a Qwen token and a Claude token process different amounts of text, so raw token volumes cannot be ranked against each other as a measure of actual workload or market share.

The Right Way to Compare Models

For any enterprise or investment analysis, the following metrics are meaningfully superior to token counts or listed prices:

Effective cost on your actual prompts: Run identical prompt batches through each model's official token-counting API, measure actual token consumption, then multiply by list price. This is the only valid cost comparison.

API call volume/request count: Tokenisation-agnostic, this measures how much work each model is being asked to do, regardless of how it slices text.

Cost per completed task: Normalise against a fixed benchmark of representative tasks (text summarisation, tool calls, code generation, multilingual queries) to compute true cost per unit of useful output.

Investment implication: Token usage rankings on OpenRouter are not a proxy for AI market share, model quality, or developer preference. For competitive positioning analysis, the more relevant data points are direct API revenue (opaque for private companies), enterprise contract wins, and proprietary benchmark performance on standardised task sets.

Sources: OpenRouter (April 2026); MBI Deep Dives; TensorZero;

Disclaimers:

This article expresses the author's views as of the date indicated on the publication and such views are subject to change without notice. Gratus has no duty or obligation to update the information contained herein. Certain statements contained herein constitute forward-looking statements, which are subject to known and unknown risks, uncertainties, and assumptions. Actual events or results may differ materially from those reflected or contemplated in such forward-looking statements. Further, Gratus makes no representation, and past investment performance should not be assumed to indicate future results. Moreover, wherever there is a potential for profits, there is also the possibility of loss. This publication is made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services, a recommendation to buy or sell any securities or related financial instruments in any jurisdiction. Any reference to specific companies or securities is for illustrative purposes only and may not represent actual holdings of any Gratus’ portfolio. Certain information contained herein concerning economic trends and performances is based on or derived from information provided by independent third-party sources. Gratus Investment Management Private Limited (“Gratus”) believes that the sources from which such information has been obtained are reliable. However, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumption on which such information is based. This publication, including the information contained herein, may not be copied, reproduced, republished or posted in whole or in part in any form without the prior written consent of Gratus. Accordingly, neither we nor any of our associates, directors, connected parties and/or employees accept any liability whatsoever for any loss, whether direct or indirect, that may arise from the use of information or opinions provided.

Related Insights